Published October 30, 2025

Mortgage Rates Drop to Footing Not Seen in a Year

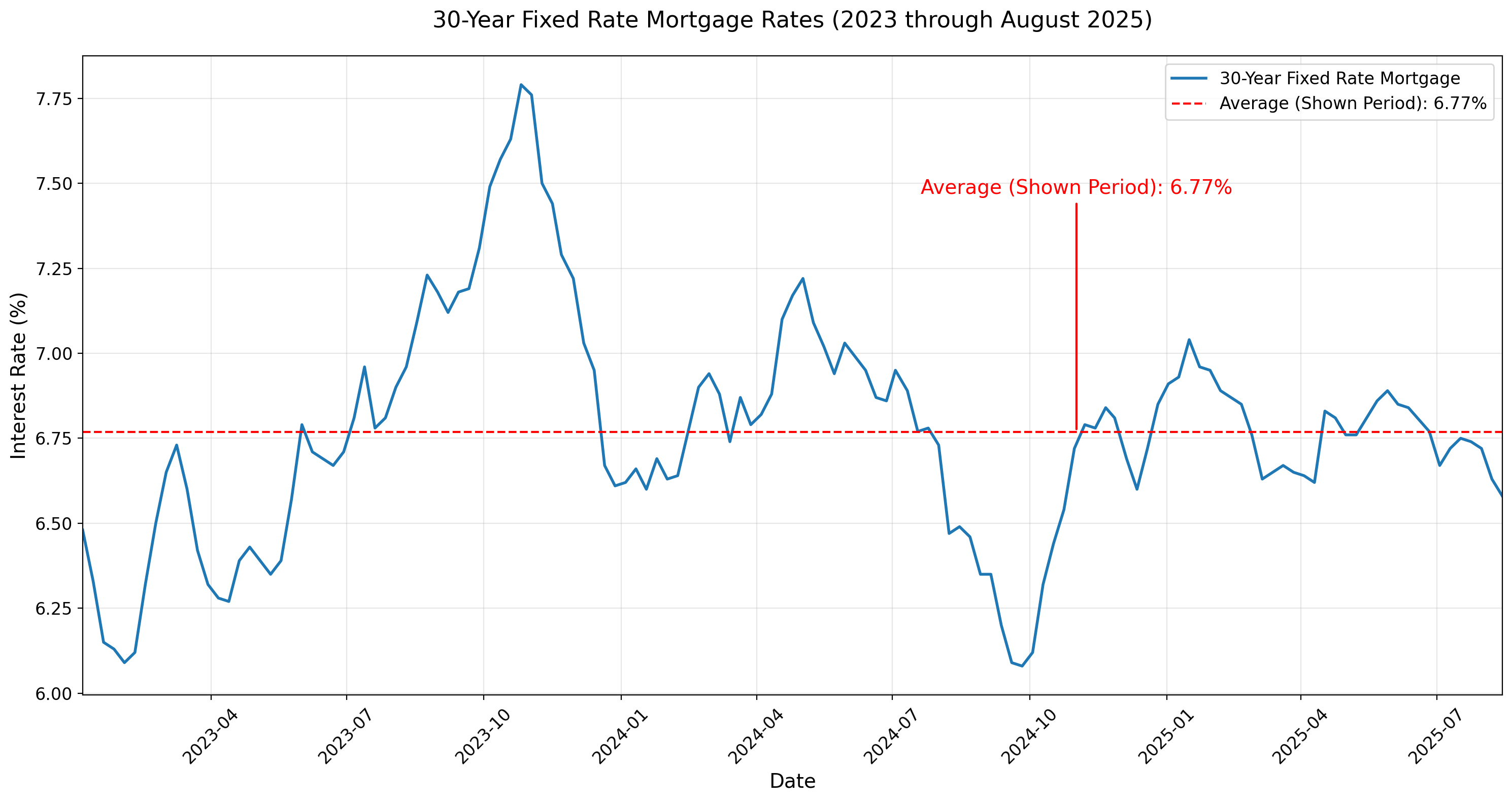

In recent weeks the average 30-year fixed mortgage rate in the U.S. has edged down to its lowest levels in about a year. According to one survey, the 30-year fixed rate averaged 6.25 %, down from higher levels earlier in 2025. Bankrate+2morningstar.com+2

Another data point shows some lenders reporting rates as low as around 6.17 % for 30-year fixed loans. morningstar.com+1

This drop is notable given the backdrop of elevated rates over the past several years.

Several factors are contributing to this decline:

-

Market expectations of future economic softness are lowering yields on U.S. Treasuries, which in turn helps mortgage rates. Bankrate+1

-

The Federal Reserve has signaled rate cuts in its benchmark policy, which influences borrowing-cost expectations. Kiplinger+1

-

A slight increase in housing-market activity is also prompting lenders to compete for buyers. National Association of REALTORS®+1

This sets the stage for important implications for homebuyers and home sellers alike.

1. Improved Affordability

When the mortgage rate drops, the monthly payment falls (all else equal), which increases how much home a buyer can afford, or reduces the burden of the payment for the same size home. For example, recent rate-drops to under 6.5 % have opened doors: According to National Association of REALTORS® (NAR), the 30-year fixed rate recently averaged about 6.30 %, providing “more opportunities for hopeful home buyers.” National Association of REALTORS®+1

A study cited by NAR showed that some rate drops over the past year could save a buyer tens of thousands of dollars over the life of a loan. National Association of REALTORS®

2. More Buyer Activity

With lower rates, sidelined buyers may re-enter the market. The interest cost is lower, and the “lock-in effect” may ease for some. For instance, as buyer activity rises, competition may increase in certain segments. CBS News+1

That said: the increase in activity isn’t automatic or evenly distributed across markets.

3. Strategic Timing Decisions

Buyers have to decide whether to act now or wait for potentially lower rates. But there’s risk: rates may not drop substantially further, and home-prices may already reflect some of the improvement in borrowing costs. Some analysts caution that while rate drops help, they’re not a panacea for affordability issues. Investopedia+1

For buyers, the key questions become:

-

How far might rates fall further?

-

What will home-prices and supply do in response?

-

How strong is one’s own financial readiness (credit score, down payment, debt load)?

-

Inventory remains constrained: Many markets still suffer from low inventory relative to demand, which keeps price-pressures elevated. Even with more buyers entering (due to lower rates), if supply doesn’t loosen, prices may stay high. Bankrate+1

-

Affordability is multifaceted: While rate drops improve affordability, home-prices, taxes, insurance, maintenance, and required down payments all factor. Some analysts caution that unless rates fall substantially, affordability gains might be modest. Investopedia

-

Regional variation is strong: What’s happening in a high-cost metro may differ dramatically from more modest markets. Buyer behavior, inventory, local economy, and financing norms vary by location.

-

Economic risk remains: If inflation resurges, or the economy weakens significantly, rates could move differently than expected. Mortgage-rates don’t move solely on the Fed’s policy; they are influenced by bond markets and investor sentiment. Bankrate+1

-

Expectations matter: Both buyers and sellers are watching for what will happen next. If many buyers expect rates to go even lower, they may delay purchases — even though a good rate is available now. Simultaneously, some sellers may wait for “ideal” pricing or market conditions, which slows market fluidity.

What This Means for You (Practical Takeaways)

-

If you’re a buyer:

-

It may be a good time to lock in a mortgage rate, especially if you’ve been waiting for a meaningful drop. The current levels reflect one of the better windows in the past year.

-

Shop around: small differences in rate and fees add up, especially over 15–30 years.

-

Don’t rely solely on the rate drop; make sure your budget is comfortable with maintenance, taxes, and other home-ownership costs.

-

Consider timing: if inventory is rising, you may have more choices; if it’s still tight, act decisively but prudently.

-

-

If you’re a seller:

-

Highlight to potential buyers the improved financing environment (i.e., lower rates = lower monthly payments) as a selling point.

-

Be realistic about pricing relative to your local market. A good financing environment doesn’t guarantee a premium price if supply is weak or buyer demand still muted.

-

If you’re also buying another home, evaluate how your own financing cost will behave — you may be trading a low-rate loan for one at a higher rate. Factor that into your decision to list/sell.

-

If you’ve been holding off listing because of rate concerns, now may be the moment to revisit your timing — but stay mindful of regional buyer demand and inventory trends.

-

-

-

Shelby Buehler

Operator | The Buehler Group | Keller Williams | PLACE

or another way